How Much Does Cyber Insurance Cost in India?

The average cost of cyber insurance depends on your business size, the type of high-risk data you handle, and the coverage amount you choose.

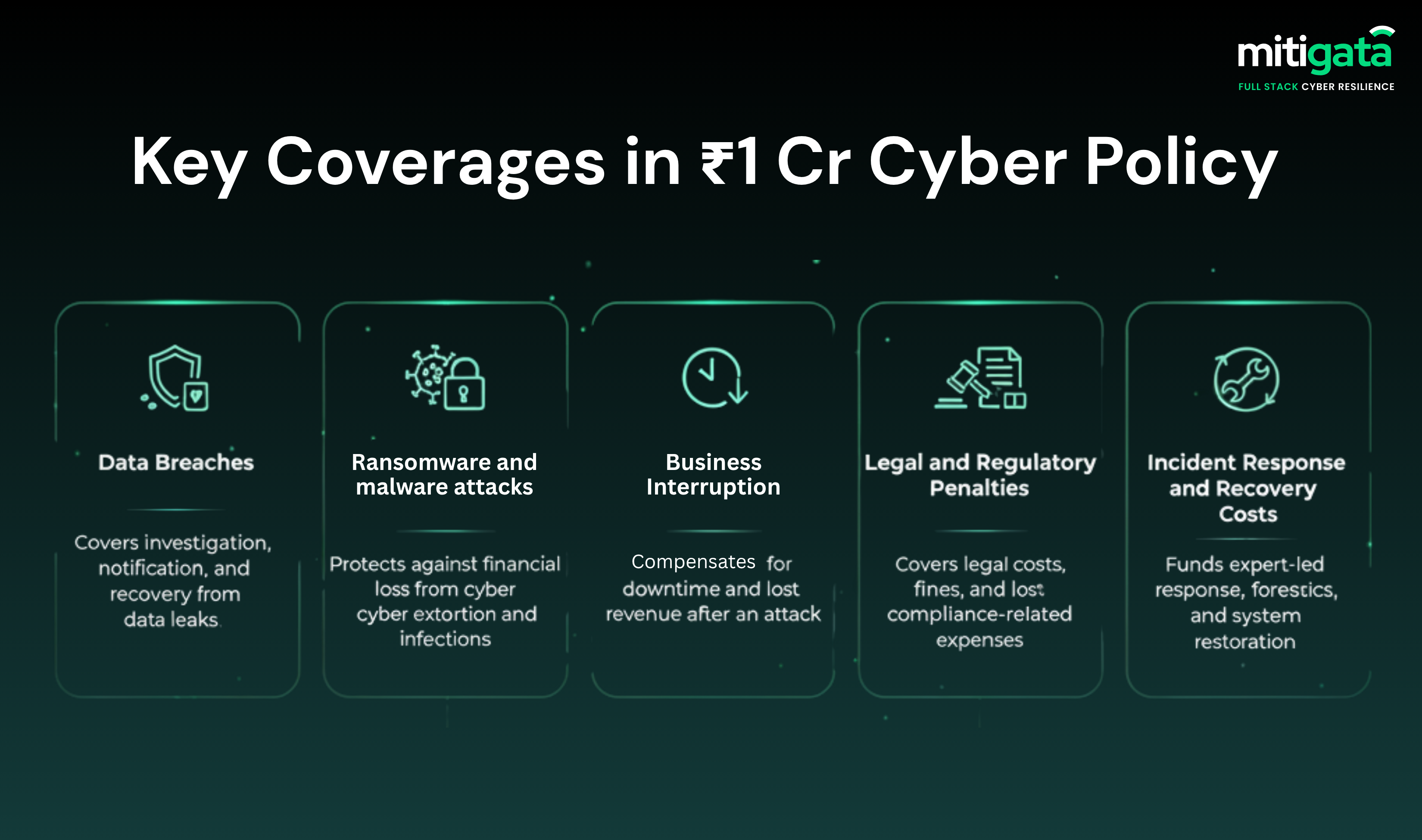

Partnered with leading insurers, Mitigata offers you a comprehensive cyber insurance coverage of ₹1 crore starting at just ₹95,000/year*.

This plan generally covers a wide range of cyber risks, including data breaches and ransomware attacks, as well as the costs of business downtime and incident response.

For larger businesses operating across multiple digital platforms and multiple regions, the coverage premium tends to scale upward depending on the risk factor.

The average cyber insurance premium for Indian businesses can range from ₹80,000 to ₹3,00,000 annually. Again, this highly depends on the scope of protection and business category.

What is Cyber Insurance?

Cyber insurance is a type of insurance for businesses to recover from financial losses caused by cyberattacks, data breaches, and other digital security risks.

We all have witnessed India’s sudden and major shift toward adopting digital payments and cloud-based systems.

The need and the demand for cyber insurance in India have broken records in 2024. The market value of cyber risk insurance in India was estimated at approx. USD 582.2 million.

What’s Covered Under Cyber Insurance

Data Breach Costs: The policy covers the costs of addressing affected users, restoring company records, and meeting legal or regulatory responsibilities.

Ransomware Payments and Negotiation Costs: Insurance covers ransom payments and the cost of employing professionals to tackle cyber extortion cases.

Business Interruption: It helps to compensate for lost income and other business interruption costs.

Reputation Management: The policy addresses crisis communication and public relations support to reestablish brand credibility following a cyber event.

Know more about cyber insurance and it’s coverage in this expertly curated guide.

What’s Not Covered

Known Incidents: Any breaches or vulnerabilities identified before the policy start date.

Intentional or Fraud Acts: Damages caused deliberately by employees or management.

Non-Cyber Failures: Events like power outages or hardware failures unrelated to a cyber event.

Which Factors Drive Cyber Insurance Premiums in India?

The cost of cyber insurance in India depends on several factors:

- Company Size and Revenue

In comparison, larger companies have more staff (and tend to have more digital assets), which makes them more likely to be victims of phishing, data theft, or system penetration, and thus have a higher rate for cyber insurance.

For example, A SaaS-type company with a team size of 50 members might pay ₹90,000 for ₹1 crore worth of insurance, while a fintech-type company with 500 employees might pay over ₹2,00,000 for the same type of insurance.

Clearly, the bigger the company, the higher the likelihood of breaches.

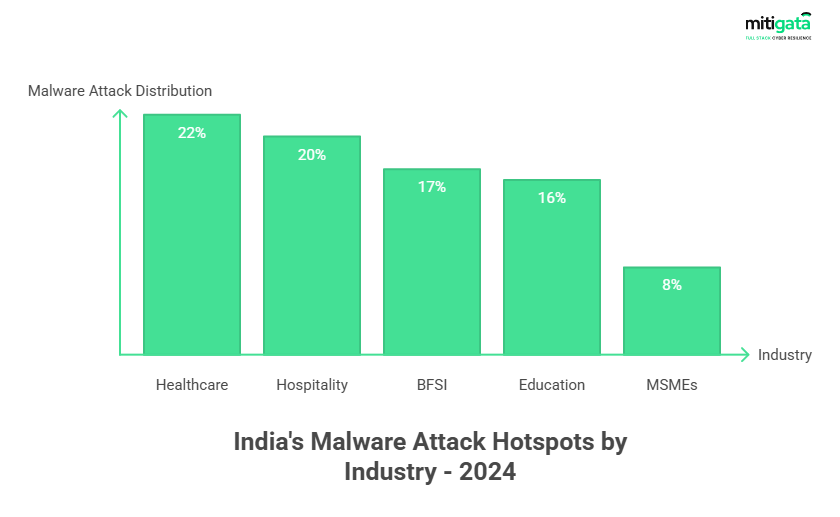

- Industry Type

Some industries are inherently more attractive to cybercriminals. Healthcare is the most targeted industry, accounting for about 21.82% of all cyber threats detected in India. This is followed by the hospitality and BFSI industries, respectively.

- Data Sensitivity and Volume

The more confidential data a company stores, the more it costs to insure. Businesses that handle online transactions daily fall under high-risk categories since they store personal identifiable information (PII) and credit card details of clients.

A fintech company managing payment transactions always has greater liability than other industry firms.

- Cybersecurity Readiness

Insurers thoroughly assess your security risk posture. Businesses that invest heavily in advanced cybersecurity controls often have reduced premiums.

Even if you have firewalls, endpoint detection, multi-factor authentication and conduct routine audits along with phishing training for employees, the overall cyber risk insurance costs will be lower for you.

Firms that can demonstrate compliance with frameworks, such as ISO 27001 or the NIST framework, may receive better premiums, as they demonstrate a measurable commitment to controlling cyber risk.

Still confused about buying cyber insurance? Read this article and explore the top proven benefits of cyber insurance.

Coverage Limits and Deductibles Explained

If you’re purchasing a cyber insurance policy, two elements determine how much protection you’ll receive:

- Coverage Limit

The coverage limit sets the maximum that your insurer will pay out on your behalf for claims resulting from a cyber incident.

For instance, if your coverage limit is ₹1 crore, but your data breach results in ₹1.2 crore worth of damages, the insurer will only pay up to ₹1 crore, and you will pay the remaining ₹20 lakh of damages.

Choosing the appropriate limit is determined by your company’s size, the sort of data it handles, and the potential financial consequences of a breach.

- Deductible

The deductible is the amount you must pay out of pocket before insurance coverage begins. A greater deductible typically results in a lower premium, but it also increases your initial financial liability following an occurrence.

For instance, if your deductible is ₹5 lakh and you experience a ₹50 lakh cyber loss, your insurer will cover ₹45 lakh.

Finding the appropriate balance between coverage and deductible is important. Most businesses in India opt for a ₹1 crore limit and a ₹2–5 lakh deductible as a reasonable and affordable option.