Did you know that roughly 40% of Professional Indemnity (PI) insurance claims in India are denied because of problems regarding the documentation provided in support of their claim?

Like delays in notifying their insurer of the claim, or misinterpretation of the PI insurance policy. This may cause lost income, increased litigation risk, and damage to professional reputation for many professionals.

A sudden rejection of the claim can leave individuals, such as consultants, accountants, architects, and service firms, shattered, as they thought their policies would protect them.

In this blog, we will discuss the most common reasons why PI insurance claims get denied and provide practical ways to minimise the risk of a claim being denied later on.

Mitigata, India’s Trusted Partner for (PI) Professional Indemnity Insurance

With over 800 businesses across 25 industries placing their trust in us, Mitigata has become India’s leading full-stack Cyber Resilience and Insurance Partner.

By collaborating with top insurers such as HDFC ERGO, ICICI Lombard, and Bajaj Allianz, we deliver the most relevant and reliable coverage without the confusion of endless comparisons or hidden exclusions.

Why over 800 businesses trust Mitigata:

- Competitive pricing with comprehensive coverage that truly protects against professional risks.

- Direct access to insurers who understand your specific industry and exposure areas.

- End-to-end support from quotations and policy setup to documentation and renewals.

- Immediate claim assistance that eliminates red tape and accelerates resolution.

- 24/7 availability because professional risks don’t follow business hours.

Get ₹5CR of Professional Indemnity

At ₹75,000/Year*

Professional indemnity cover at ₹75,000 per year saves you money while keeping your practice safe.

Understanding PI Insurance Claims

Professional Indemnity insurance (PI) is an insurance policy that protects a professional against losses resulting from errors, omissions or negligence in the professional services provided.

PI insurance payouts will cover legal costs, settlement amounts, and compensating clients for damages if professional advice or actions caused injury.

Even though professional indemnity insurance is primarily associated with traditional professions such as consultancy, chartered accountancy, engineering, architecture, IT firms and marketing companies, it is important for anyone providing a professional service.

But obtaining a professional indemnity policy is just the first step in the process of providing your client with coverage. There is still a process to follow to have your claim accepted. It is essential to get the details right by being precise in terms of time and to follow the insurer’s directions.

Even missing a small detail in the policy conditions or misunderstanding them can cause a PI insurance claim to be denied.

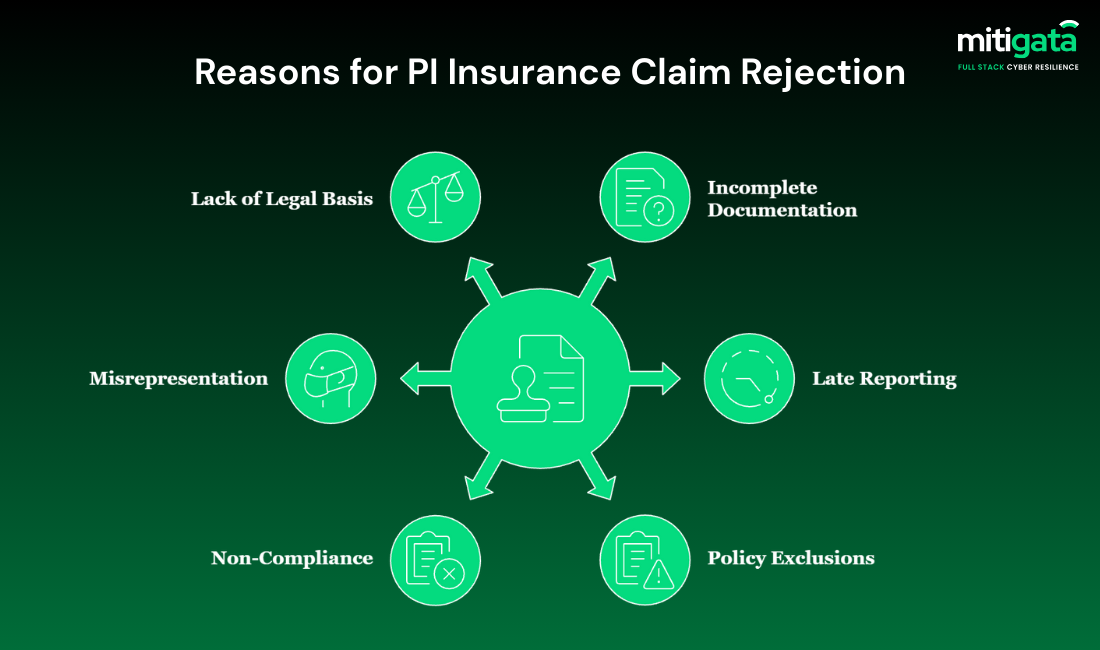

Top Reasons Why PI Insurance Claims Get Rejected

Professional Indemnity (PI) Insurance claims get rejected a lot due to silly mistakes that are actually avoidable. Here are the most commonly made mistakes that you can avoid to minimise the risk.

- Incomplete or Incorrect Documentation

Missing or unusual documentation is one of the primary reasons that PI claims are denied. Insurers expect detailed proof of professional negligence, including client engagement letters, invoices, email correspondence, and records of client communications.

If these documents are missing, inconsistent or not provided by the insured, the insurers will often deny the claim entirely.

- Late Reporting of the Incident to the Insurer

A PI claim is more often rejected by an insurance company because the incident was not reported in accordance with the policy terms. Most PI policies require potential claims to be reported immediately upon the insured becoming aware of the claim or a potential error.

If the insured waits to respond until receiving a legal claim or if the issue raised escalates, the claim would typically be automatically denied.

Want to know more about how professional indemnity insurance premiums work? Then, check out our expert-curated guide on it.

- Exclusions and Limitations in Policy

The rejection of claims by many businesses stems from the policyholder’s misunderstanding of the coverage’s scope. It includes actions that are both reckless and intentional, or any actions being performed for a different legal entity.

Misreading or ignoring these exclusions at the time of application during the renewal process can lead to a misunderstanding, resulting in a claim being denied.

₹5 Crore Professional Indemnity Cover Starting at ₹75,000/Year*

With Mitigata, you’re never alone, our 24/7 assistance helps resolve claims and concerns without waiting.

- Failure to Abide by Conditions of Policy

Every PI policy includes certain obligations, such as quality control, client documentation, and professional licensing/registration. If any of these obligations is not fulfilled, the insurer may deem it a failure to comply with the policy conditions.

- Previously Known / Misrepresentation

Overlooking previous issues related to complaints or lawsuits on the application will influence the result of the PI insurance claim. On application, insurers expect to know about any prior incidents or information that may generate a claim. Not disclosing this information leads to misrepresentation and may result in the rejection of the policy in its entirety, regardless of whether it was intentional.

In many cases, claims lack the necessary legal basis or fail to establish professional negligence. If there is no direct connection between the alleged professional error and the professional’s actions, the insurer may deny the claim. Claims that are circumstantial or lack documentation are habitually denied.

How to Avoid PI Insurance Claim Rejections

While many professional indemnity insurance claims are denied, many rejections could have been avoided. By following this, your business could improve the chances of approval:

Be detail-oriented: Keep contracts, emails, reports, and any client engagements organised and accessible.

Report possible claims: Inform your insurer at the first sign of a claim, whether it’s formally filed or not.

Review exclusions: Each year, ensure your coverage still aligns with your coverage and services.

800+ Businesses Trust Mitigata For Protection That Never Misses The Mark

Get PI insurance powered by top insurers and proven expertise that delivers value and security every day.

Engage specialists: The professionals who are experts in PI or cyber insurance will ensure your claim and policy are aligned with the requirements of your insurer.

Audit your compliance and documentation: Periodically use auditable records to review your risk and record-keeping to eliminate the risk of accidental breach.

These next steps of proactivity will help ensure that your PI insurance operates as intended when you need it most.

Conclusion

Most PI insurance claims are rejected due to errors that could have been avoided, including late notification of the claim, incomplete documentation, and misinterpretation of the policy. With the right advice, you can eliminate these problems before you put your business at risk.

Mitigata will ensure your policies are compliant, your claims are defensible, and your business’s reputation is protected.

Partner with Mitigata and get a PI insurance quote in minutes!