In 2026, it just takes one weak checkout link to bring down an Indian e-commerce business.

The cyber losses are expected to cross ₹20,000 crore, and AI-driven attackers are relentlessly exploiting misconfigured payment gateways and ignored PCI gaps.

A single lapse can trigger data theft, payment shutdowns, regulatory penalties, and irreversible loss of customer trust.

That’s where PCI DSS compliance stands as the frontline defence that closes these cracks and protects your accounts.

Mitigata – India’s Leading Cyber Resilience Company

Our unified platform helps retailers and payment-handling businesses manage the entire PCI DSS lifecycle, from scope definition to audit, without disrupting operations.

Over 800+ businesses across 25+ industries trust Mitigata to simplify PCI compliance, reduce card-data risk, and stay ready for assessments year-round.

Here’s what our PCI compliance platform offers:

Automated PCI Compliance – Automates evidence collection, control checks, and remediation tracking.

Card Data Risk Management – Real-time visibility into risks across cardholder data systems.

Centralised Documentation – All PCI policies and audit evidence in one secure place.

Expert-Led PCI Support – 24/7 guidance for scoping, remediation, and audits.

Security Awareness Training – Free PCI training for teams handling card data.

PCI-Focused VAPT – Vulnerability and penetration testing aligned with PCI DSS.

Why Mitigata?

Unlike generic GRC tools, our platform is specifically engineered for the Indian regulatory landscape, ensuring your compliance aligns not just with global standards but also supports RBI’s Digital Payment Security Controls.

One platform to Manage governance, risk, and compliance.

Track open risks, control status, vendor assessments, and audits instantly with Mitigata’s cost-effective and scalable GRC platform.

What Is PCI Compliance?

PCI DSS (Payment Card Industry Data Security Standard) is a global set of security standards designed to ensure that companies handling credit card information maintain a secure environment.

Currently transitioning to PCI DSS v4.0, the standard now focuses on continuous security rather than just a ‘point-in-time’ annual check.

This shift is crucial for Indian SMEs digitising their payments rapidly.

Example :

When a customer pays at a store, their card number is automatically encrypted and never saved in plain text.

Only approved systems can access the payment process, so even if hackers gain access, they can’t read or misuse the card data.

Who Needs PCI Compliance? Retail and E-commerce Breakdown

PCI DSS compliance is mandatory for any entity that processes, stores, or transmits cardholder data from major brands like Visa, Mastercard, and American Express.

This applies regardless of the size of your business or the number of transactions you process.

Whether you are a local kirana store using a modern POS or a D2C brand on Shopify, compliance is non-negotiable.

Coverage Areas:

Online payments: E-commerce websites and marketplaces. (including those using payment aggregators like Razorpay or PayU).

Mobile apps: In-app purchases via card.

POS systems: Brick-and-mortar retail terminals.

Call centres: Phone-based card transactions.

Email invoices: Links or details for card payments.

Discover how GRC strengthens your overall cyber strategy before gaps turn into risks.

12 PCI DSS Requirements: The 2026 Checklist for Retailers

Here’s a list of the requirements that retailers must meet to prevent risks and ensure smooth business operations.

| S. No | PCI DSS Requirement | What It Means in Retail | Risk It Prevents |

|---|---|---|---|

| 1 | Secure Network Controls | Firewalls and network rules isolate payment systems from other networks | Exposed POS systems, open payment servers |

| 2 | Remove Vendor Defaults | Change default passwords and settings on POS, routers, plugins, and cloud tools | Easy account takeovers using known credentials |

| 3 | Protect Stored Card Data | Encrypt or tokenise stored card data, or avoid storing it altogether | Large-scale data theft, compliance penalties |

| 4 | Encrypt Data in Transit | Use strong encryption for checkout pages, APIs, mobile apps, and gateways | Intercepted card data during transactions |

| 5 | Active Malware Protection | Deploy endpoint security, script monitoring, and file integrity tools | Card-skimming malware, POS infections |

| 6 | Secure Systems & Apps | Patch software, update plugins, and scan for vulnerabilities regularly | Exploits targeting outdated systems |

| 7 | Restrict Data Access | Grant card data access strictly based on job roles | Insider misuse, accidental exposure |

| 8 | Unique IDs & MFA | Assign individual user IDs and enforce multi-factor authentication | Untraceable actions, shared-account abuse |

| 9 | Limit Physical Access | Secure servers, POS devices, backups, and network equipment | Hardware tampering, data theft via physical access |

| 10 | Log & Monitor Access | Record and review system activity and data access continuously | Undetected breaches, delayed response |

| 11 | Regular Security Testing | Run vulnerability scans and penetration tests, especially after changes | Hidden security gaps, false sense of safety |

| 12 | Updated Security Policies | Maintain clear, reviewed policies for payment data handling | Inconsistent practices, compliance failures |

1. Install and Maintain Secure Network Controls

This requirement is implemented to prevent payment systems from being directly accessible. Firewalls and network rules will determine who is allowed to access your payment systems and who is not.

In modern cloud environments (like AWS or Azure), this also refers to ‘Security Groups’. You must ensure there is a ‘DMZ’ (Demilitarised Zone) that separates your public-facing web server from your internal database containing sensitive data.

IT security incidents often occur when payment traffic is treated as originating from other untrusted systems, which is why breaches happen.

2. Remove Vendor Default Settings

Default settings are an open invitation. Devices such as:

- Routers

- POS devices

- Plugins

- admin panels

- Cloud services

Often come with known usernames and passwords (e.g., admin/admin123). Attackers target default credentials and settings first, so PCI requires that all defaults be changed to match your business’s actual operating practices.

Practical Tip: Create a ‘hardening guide’ for your IT team that mandates changing credentials immediately upon unboxing any new hardware or spinning up a new server instance.

3. Protect Stored Cardholder Data

Storing card data increases responsibility and risk. If card numbers are retained in your systems, PCI expects strong encryption or tokenisation.

Many retailers reduce risk by not storing card data at all and letting payment providers handle it.

If storage exists, it must be limited, protected, and justified. Old data that no longer serves a business purpose becomes a liability.

Under the new Digital Personal Data Protection (DPDP) Act in India, holding unnecessary customer data can also lead to severe regulatory penalties, making this requirement doubly important.

From Policy to Proof, Manage Everything in One Place.

Mitigata GRC streamlines compliance tasks so you save time, reduce errors, and focus on what really matters.

4. Encrypt Cardholder Data During Transmission

Data is most vulnerable while moving. Whenever card data travels across public networks, encryption must protect it.

This includes checkout pages, APIs, mobile apps, and integrations with payment gateways.

Weak or outdated encryption exposes transactions to interception, even when everything else looks secure.

Ensure your website uses TLS 1.2 or higher; older protocols like SSL are no longer considered secure.

Example: Ticketmaster / Live Nation data breach:

In 2024, Ticketmaster confirmed a major data breach in which attackers accessed phone numbers and credit card data for about 560 million customers through a third-party vendor (Snowflake).

It showed how weak controls around payment systems and vendors can lead to massive PCI DSS failures, even for large global brands.

5. Use Active Malware Protection

Malware targets payment environments immediately. Attackers commonly use tactics such as installing malicious scripts that capture card information from checkout pages or POS systems (a technique known as ‘digital skimming’ or ‘Magecart’ attacks).

The PCI requirement states that compromised systems must use tools that are efficient in detecting and stopping such activities through endpoint protection and file integrity monitoring.

This requirement is to track threats before customers are affected.

Practical steps to build an effective GRC program that reduces risk and improves controls.

6. Maintain Secure Systems and Applications

Unpatched systems are a direct invitation to attackers. Once a software issue is disclosed, it becomes open to the public and is easy to exploit.

PCI wants retailers to apply regular updates, scan for vulnerabilities, and adopt secure development practices to eliminate potential threats.

In the case of online stores, this usually involves plugins, themes, APIs, and custom code that quietly get neglected.

For Indian e-commerce sites running on Magento or WordPress, failing to update a single plugin is the no.1 cause of compromise.

7. Limit Access to Cardholder Data

Access to payment data is not necessary for everyone. PCI insists that access should align with job roles.

Support teams, developers, marketers, and finance staff should view only what they need.

Fewer access points result in fewer chances of making mistakes or misuse. This control frequently shows how much unnecessary access has been built up over time.

This is the principle of ‘Least Privilege’ or identity access management. For instance, a marketing manager needs customer emails, but they do not need access to transaction IDs or partial card numbers.

8. Assign Unique User IDs and Authentication Controls

Shared accounts are not a good practice as they mask accountability. Everyone accessing the systems with card data must have their own unique ID.

This is further reinforced by multi-factor authentication (MFA). PCI DSS v4.0 now mandates MFA for all access to the Cardholder Data Environment (CDE), not just for remote access.

When something goes wrong, the logs should clearly indicate who did what and when. This requirement is beneficial for both security and investigation.

9. Limit Physical Access to Payment Systems

Digital security is still largely about controlling the physical environment.

- Servers

- POS terminals

- networking devices

- backup drives

They must all be secured against unauthorised entry. PCI requires measures such as locked rooms, access monitoring, and written procedures.

Physical vulnerabilities can often negate the effect of high-quality digital protections.

Case Study: A retail chain in Mumbai suffered a breach when a rogue employee simply plugged a keylogger into an unguarded POS terminal USB port. Physical locks on ports could have prevented this.

PCI Compliance - Simplified for Your Business

From scope to audit, manage PCI DSS smoothly with automated controls and 24/7 guidance.

10. Record and Oversee all Access

Security incidents rarely announce themselves. Logging and monitoring reveal patterns that humans cannot detect.

PCI requires retailers to not only document access to their systems and card data but also evaluate that activity.

Odd behaviour, unsuccessful logins, or unexpected changes in the system often indicate early warning signs.

Using a SIEM (Security Information and Event Management) tool can automate this by alerting you instantly if, for example, a user tries to download the entire transaction database at 3 AM.

11. Conduct Regular Security Tests

Continuous testing turns assumptions into verified facts, ensuring defences stay effective as systems and technologies change.

Run regular vulnerability scans to identify known weaknesses early.

Conduct periodic penetration testing to validate real-world attack paths.

Re-test systems after platform updates, plugin changes, or new integrations.

Don’t rely on past results; security gaps can return silently.

Discover top tools that make ISO 27001 compliance easier and more efficient.

12. Keep Information Security Policies Updated

Security is reliant on uniform conduct. Documented policies provide direction on handling payment data, assign responsibilities, and define the process for issue resolution.

PCI requires that these policies remain up to date and undergo regular review. They support teams through transitions rather than relying on guesswork in decision-making.

This includes having a clear ‘Incident Response Plan’, so your team knows exactly who to call (legal, forensics, insurance) in the first “Golden Hour” of a breach.

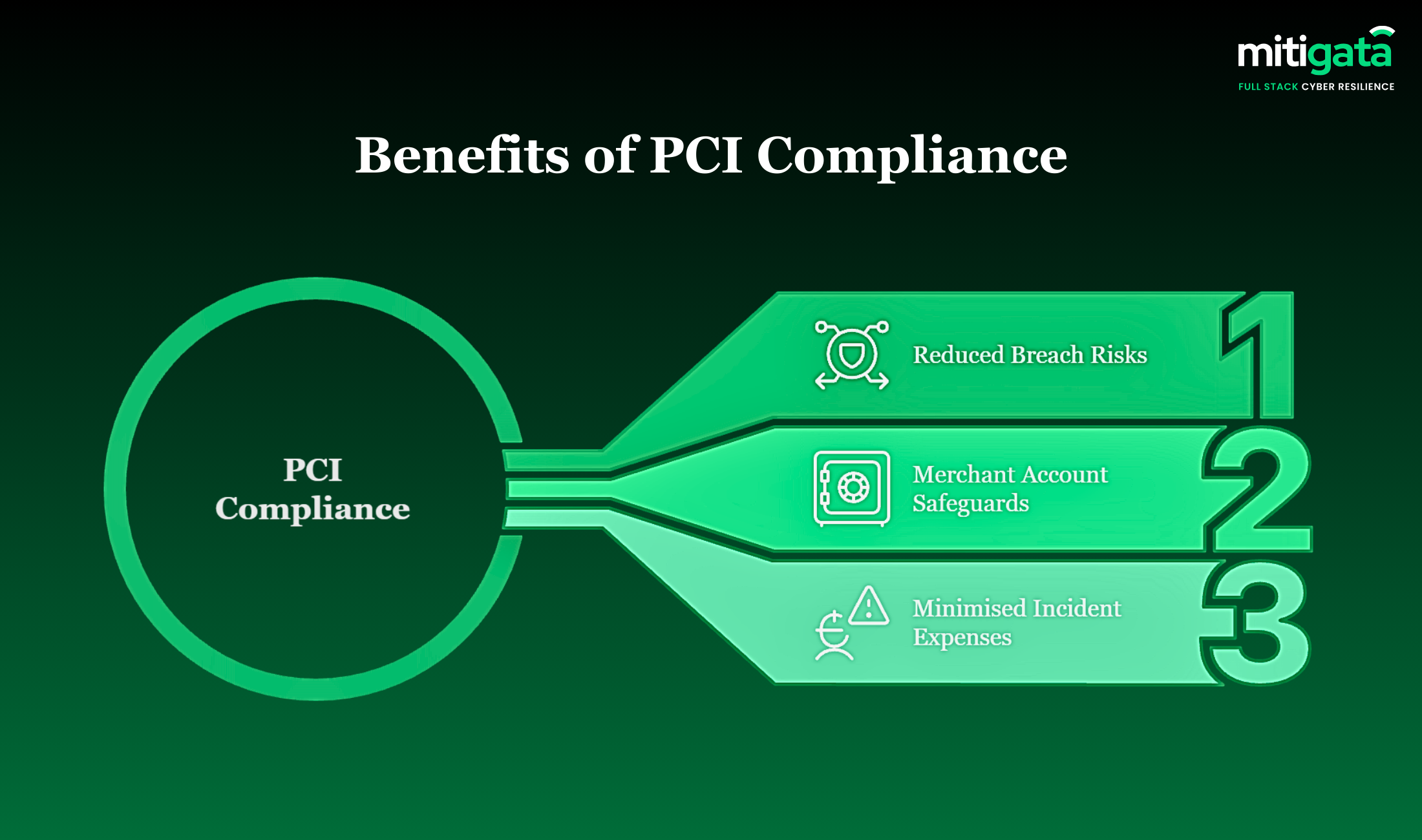

Benefits of PCI Compliance for the Retail Industry

The adoption of PCI DSS standards is not merely a regulation imposed by card companies to secure transactions, but to safeguard customer data. The following are a few PCI compliance benefits:

Reduced Breach Risks

Retail payment systems mostly fail in expected areas. Checkout pages, old plugins, and third-party scripts are common entry points for attackers.

The PCI DSS requires retailers to encrypt card data, isolate payment systems from the network, and restrict access to sensitive areas.

Merchant Account Safeguards

Card payments are the engine driving retail sales. Losing access to that payment channel could result in an immediate halt to sales.

Compliance maintains the merchant account and protects retailers from being charged fines or processing fees or being suddenly suspended.

This is especially beneficial for those retail businesses that operate both offline and online, and stability is needed across all sales channels.

Minimised Incident Expenses

Security incidents rarely end with just one fine. In the absence of PCI controls, retailers are facing escalating costs for chargebacks, forensic investigations, legal reviews, and emergency fixes.

Furthermore, being PCI compliant often lowers your Cyber Insurance premiums, as insurers view compliant businesses as lower risk.

Conclusion

When PCI DSS becomes part of daily operations, payment security remains proactive rather than reactive.

Don’t wait for a breach to be your wake-up call. Secure your customer’s trust and your business’s future today.

Contact Mitigata to keep your payment systems secure and compliant.