What if your professional indemnity insurance doesn’t step in when you need it most?

More and more professionals now recognise the need for PI insurance. Yet negligence remains the leading cause of claims, accounting for over 45% of notifications to Marsh India between 2022 and 2023.

Behind those figures are consultants, architects, and advisors who have discovered, too late, that one mistake, miscommunication, or overlooked detail could trigger serious financial losses.

The real problem is that many believe their policies have them covered when actually the coverage does not match the risks they face.

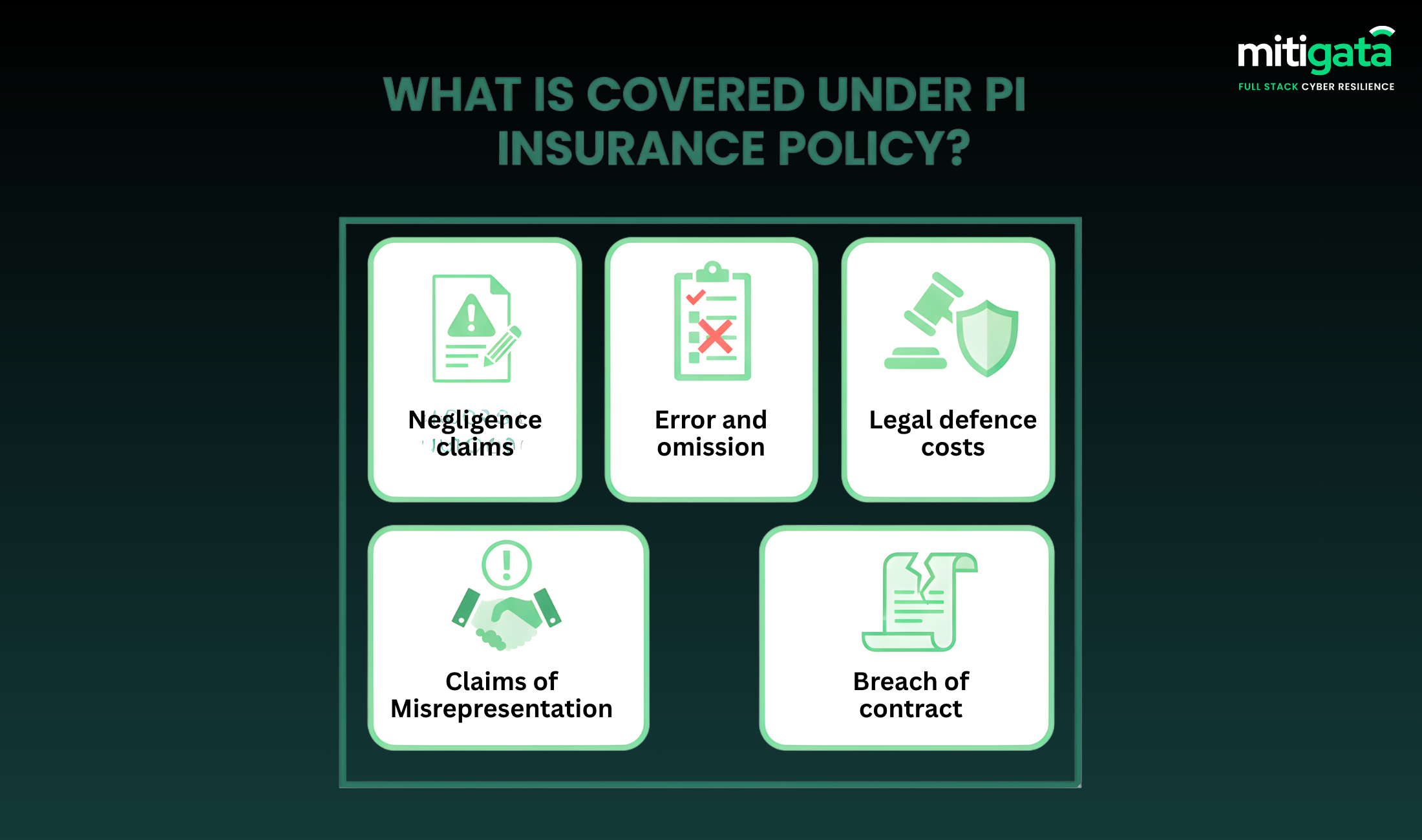

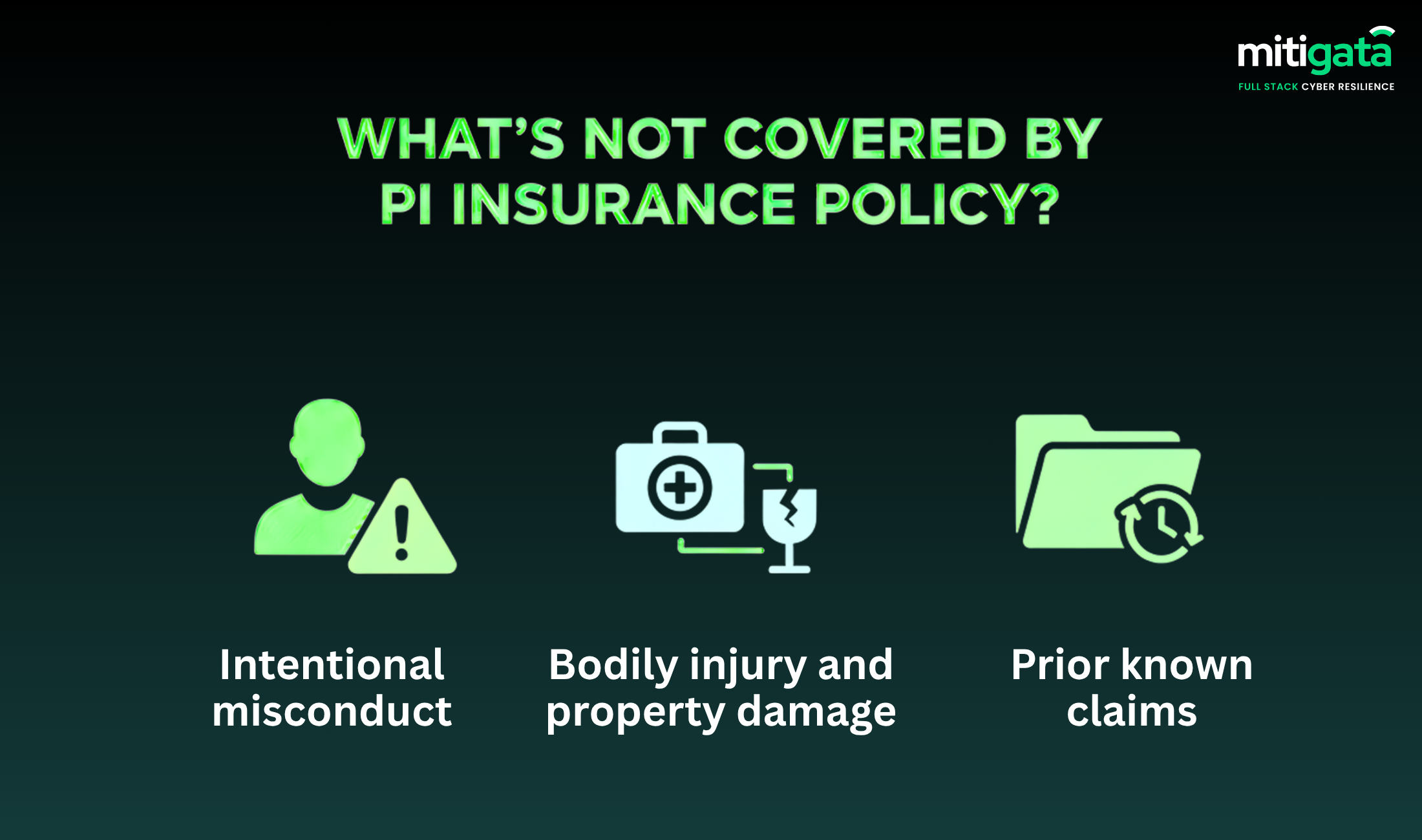

This guide will break down the inclusions and exclusions of PI insurance coverage, giving you the clarity to choose protection that genuinely safeguards your business, your finances, and your reputation.

Mitigata – Leading Professional Indemnity Insurance Provider

Choosing the right professional liability insurance coverage is not just about finding a policy. It’s about finding the right partner who understands your risks and stands by you when things go wrong.

That’s where Mitigata is the partner you need.

Trusted by over 800 businesses across 25 industries, Mitigata has established itself as India’s leading full-stack cyber resilience company. We work closely with top insurers like HDFC ERGO, ICICI Lombard, and Bajaj Allianz, giving you access to the most relevant policies without the hassle of endless comparisons.

Why do 800+ businesses choose us?

- Competitive rates with comprehensive coverage that actually protects your business without hidden gaps.

- We connect you with insurers who understand your specific industry risks, not generic solutions.

- From quotes to final paperwork, we handle everything while you focus on your business.

- When trouble strikes, we jump in immediately to cut through red tape and delays.

- Professional crises don’t follow office hours – neither do we.